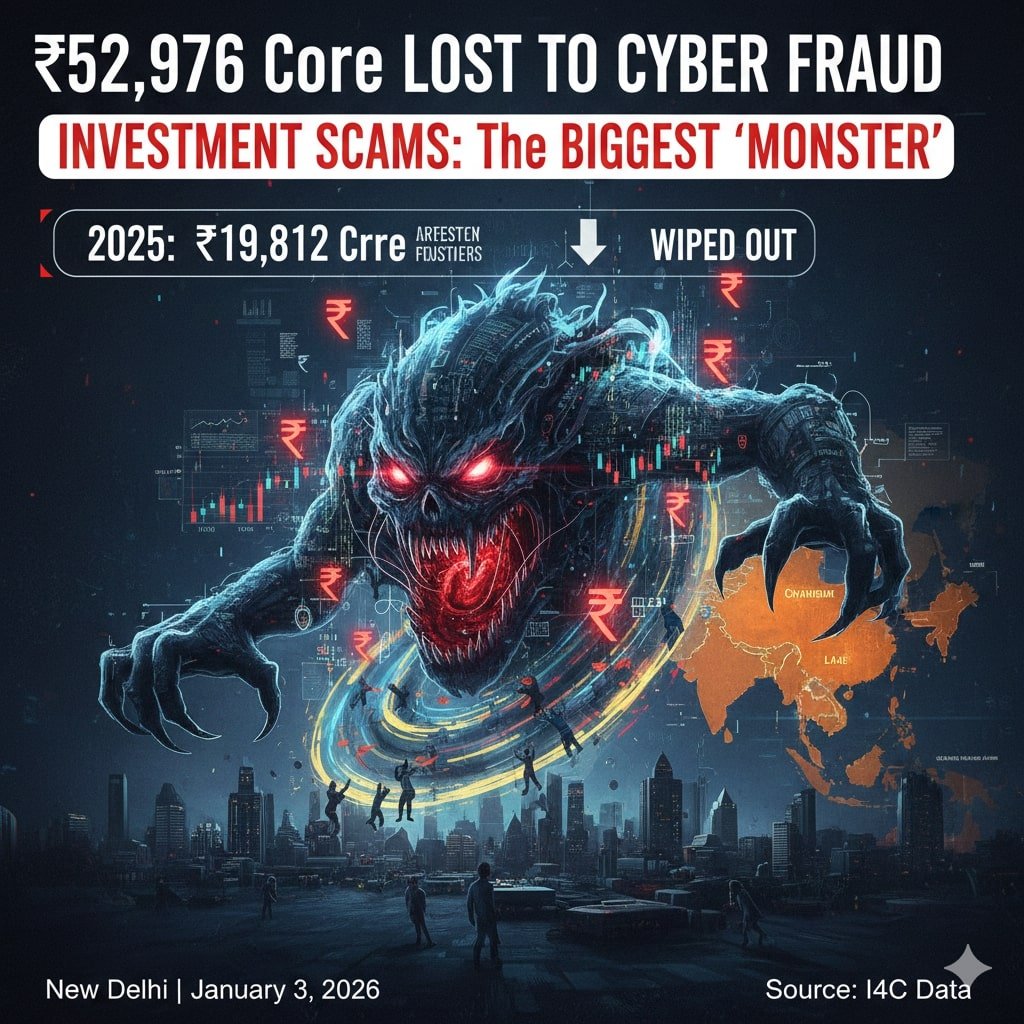

Cyber fraud in India is no longer confined to small-time scams or isolated incidents. Over the last six years (2020–2025), the country has suffered cumulative losses of ₹52,976 crore due to cyber fraud and cheating-related crimes. The data has been compiled by the Indian Cyber Crime Coordination Centre (I4C) under the Union Home Ministry, drawing from complaints registered on the National Cyber Crime Reporting Portal.

What stands out starkly is the scale of losses concentrated in the most recent year. 2025 alone accounted for ₹19,812 crore, meaning nearly one-third of the total six-year cyber fraud bill was incurred in just twelve months.

Investigators say this sharp spike signals a fundamental shift—cyber fraud has evolved into a structured, organised financial crime ecosystem, rather than sporadic digital deception.

2025: The year cyber fraud exploded

According to I4C data, over 21.77 lakh cheating-linked cyber complaints were recorded in 2025. A year-wise comparison highlights how rapidly both complaints and financial losses have surged:

- 2024: ₹22,849 crore lost; 19.18 lakh complaints

- 2023: ₹7,463 crore; 13.10 lakh complaints

- 2022: ₹2,290 crore; 6.94 lakh complaints

- 2021: ₹551 crore; 2.62 lakh complaints

- 2020: ₹8.56 crore; 1.27 lakh complaints

While 2024 shows a marginally higher loss figure, experts note that 2025 recorded a far higher complaint volume and average loss per case, indicating faster money movement, larger ticket frauds, and improved scam efficiency.

“Cyber fraud is no longer opportunistic—it is industrial,” a senior official involved in cybercrime analysis said.

Investment fraud: The biggest ‘killer’

The most alarming insight from 2025 data is the dominance of investment-related scams, which accounted for 77% of the total financial loss.

The category-wise breakup of losses in 2025 is as follows:

- Investment scams: 77%

- Digital arrest scams: 8%

- Credit card fraud: 7%

- Sextortion: 4%

- E-commerce fraud: 3%

- App/malware-based fraud: 1%

Investigators stress that victims are not merely “clicking malicious links.” Instead, they are being systematically groomed through fake trading apps, cloned investment platforms, social media ads, and self-styled “financial experts” promising high and guaranteed returns.

Which states were hit the hardest

State-wise analysis shows that regions with high digital adoption and transaction density bore the maximum losses.

Top states in 2025:

- Maharashtra: ₹3,203 crore; 28.33 lakh complaints

- Karnataka: ₹2,413 crore; 21.32 lakh complaints

- Tamil Nadu: ₹1,897 crore; 12.32 lakh complaints

- Uttar Pradesh: ₹1,443 crore; 27.52 lakh complaints

- Telangana: ₹1,372 crore; around 95,000 complaints

Together, these five states accounted for more than half of the national cyber fraud losses. Other significant contributors included Gujarat (₹1,312 crore), Delhi (₹1,163 crore), and West Bengal (₹1,073 crore).

The international angle: Southeast Asia in focus

According to research inputs from the Future Crime Research Foundation (FCRF), nearly 45% of cyber fraud activities reported in 2025 showed digital links to Southeast Asian countries such as Cambodia, Myanmar, and Laos.

FCRF’s category-wise assessment indicates:

- 36% investment fraud

- 27% credit card fraud

- 18% sextortion

- 10% e-commerce fraud

- 6% digital arrest scams

- 3% app/malware-based fraud

Law enforcement agencies say many Indian victims are targeted through calls, messages, and apps, while operations are often run from foreign scam hubs, with funds routed through layered bank accounts, shell entities, and sometimes cryptocurrency.

Why cyber fraud is growing so fast

Officials and analysts point to multiple overlapping factors:

- Rapid digitisation and explosive growth in UPI and online payments

- Professionally run scam networks with scripted calls and dedicated tech teams

- Sophisticated social engineering and psychological pressure tactics

- Expansion of fraud operations into smaller towns and rural areas

“These are no longer scattered crimes,” an investigator said. “They resemble corporate-style operations with clear role separation—recruiters, tech handlers, mule accounts, and fund managers.”

The ₹52,976 crore cyber fraud bill is not just an economic loss—it reflects a deepening crisis of digital trust. Experts argue that combating this threat will require:

- Tighter regulatory oversight of investment platforms

- Faster bank-to-police coordination

- Real-time fraud detection and alert systems

- Large-scale public awareness and financial-cyber literacy

As India’s digital economy continues to expand, the warning is clear: unless security, regulation, and awareness grow at the same pace, the cost of cyber fraud will only rise further.