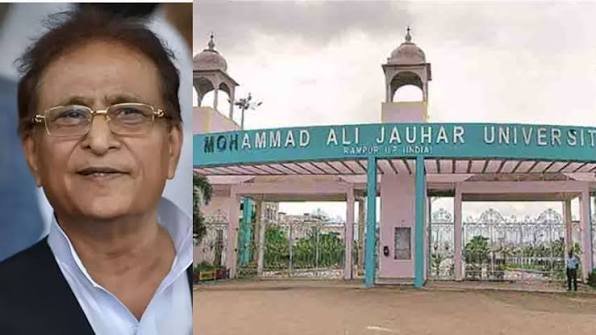

The Income Tax Department has intensified its scrutiny of Jauhar Trust, an organization linked to former minister Azam Khan and his family, by issuing a show-cause notice seeking explanations on a range of financial and administrative issues. According to officials, the action is part of an ongoing examination of alleged irregularities related to tax exemptions granted to the trust.

The trust has been directed to present its case before the department on the specified date. Failure to provide a satisfactory explanation could result in the cancellation of its registration and income tax exemption certificate under Section 12AB of the Income-tax Act.

Registration Begins for FutureCrime Summit 2026, India’s Largest Cybercrime Conference

Discrepancies in Income and Bank Deposits

The notice, issued by the Principal Commissioner of Income Tax (Central) in Lucknow, raises several critical questions concerning the trust’s activities, financial transactions, land use, construction projects, and sources of donations. The department has cited findings from previous search operations and judicial observations while seeking detailed clarification on multiple aspects of the trust’s operations. One of the central issues under examination relates directly to the trust’s financial records.

Officials claim there are massive structural discrepancies between the income declared in tax filings and the actual cash amounts deposited in the trust’s bank accounts between the financial years 2020-21 and 2023-24. According to the department, the trust declared an income of approximately ₹12.83 crore for 2020-21, whereas bank deposits totaling around ₹27.39 crore were recorded in its active statements.

Similarly, for the financial year 2021-22, the trust reported a declared income of about ₹8.31 crore, but bank deposits closing at nearly ₹25.04 crore were identified by central auditing cells.

The asset tracking loop maps these financial variables through an unverified ledger pattern. The sequence initiates with search-based scrutiny, where central enforcement actions under Section 132 uncover hidden property documents. This moves directly into ledger contrast auditing, where investigators isolate the multi-crore gaps between declared tax returns and actual current account deposits. The cycle concludes with statutory evaluation, placing the procedural burden of proof onto the trust handlers to verify the missing audit trails before formal cancellation actions are completed.

The ₹494 Crore Structural Valuation Gap

Questions have also been raised regarding the true cost of construction activities carried out within the Muhammad Ali Jauhar University campus. A detailed departmental engineering assessment estimated the total capital expenditure on 59 university buildings at approximately ₹494 crore. In stark contrast, the trust’s accounting sheets declared a spending footprint of only around ₹46 crore on those identical projects.

Given the substantial gap between the two figures, the department has demanded a comprehensive explanation along with supporting ledger entries, architect certificates, and material procurement records. The notice also refers to statements made by certain contractors during the course of the investigation, alleging that funds sanctioned under public government welfare schemes may have been illegally diverted and utilized for construction work within the private university campus.

Unverified Donors and Campus Encroachments

Donations received by the trust have emerged as another major focus of the investigation. The department has expressed deep concerns about the verification of several individual donors and the authenticity of financial records associated with them. Investigators have encountered significant difficulties in tracing certain donors whose contributions were reflected in the trust’s accounts, prompting the authority to demand independent identity verification papers.

Furthermore, the notice questions the construction of a mosque and a political party office building within the university campus boundaries, alongside the alleged occupation of regional land blocks beyond approved master plan limits. Compliance with mandatory fire safety norms and statutory municipal approvals for several blocks is also under review. With the formal issuance of this show-cause notice, the trust’s tax-exempt status enters a critical window, with the final cancellation trajectory dependent entirely on the documentation submitted before the Central Circle.