Mumbai: The Indian Income Tax (I-T) Department has begun tightening its grip on cryptocurrency traders who are allegedly bypassing the 1% Tax Deducted at Source (TDS) by using foreign platforms like Binance. This comes amid growing concerns over tax evasion and the movement of digital assets offshore.

Background: The TDS Mandate

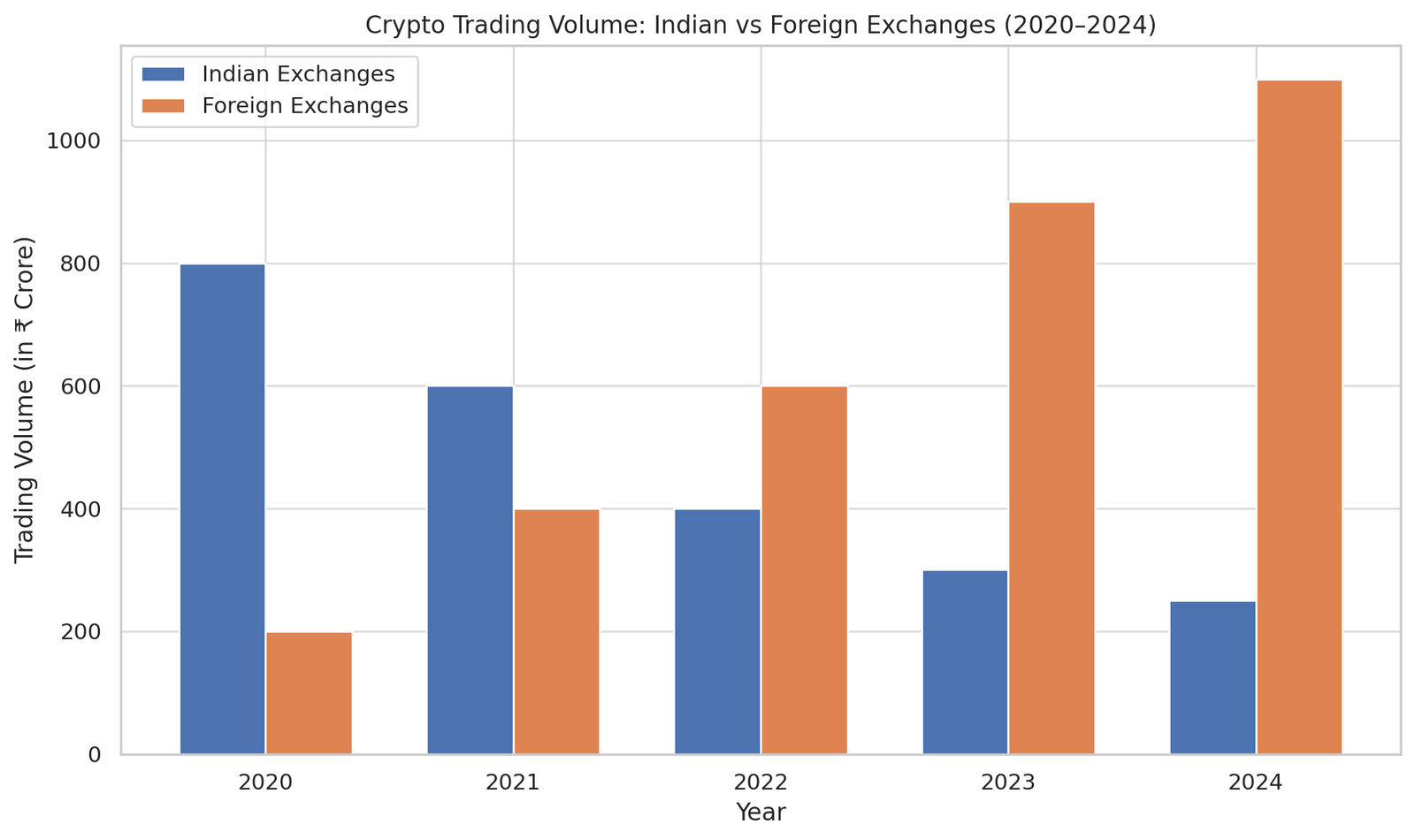

Since July 2022, the Indian government mandated a 1% TDS on all crypto transactions to bring digital assets under the tax net. This rule primarily affects transactions conducted through domestic exchanges, which are required to deduct and deposit the TDS directly with the government. However, foreign platforms like Binance are not obligated to comply with Indian tax laws, leading many Indian traders to shift their crypto holdings offshore.

Tax Evasion via P2P and Swaps

A large number of Indian users on Binance conduct peer-to-peer (P2P) transactions, where buyers and sellers settle deals in rupees via the platform. This setup bypasses the direct TDS deduction, making it difficult for authorities to track. Furthermore, crypto-to-crypto swaps—frequent among foreign platforms—also fall under TDS regulations. Both the buyer and seller are liable to deduct and pay the tax, but this is often ignored or overlooked.

Income Tax Department’s Investigation

In the past few weeks, the I-T Department has:

-

Sent notices to users asking for proof of TDS compliance

-

Sought income tax returns for years when crypto assets were acquired

-

Imposed 30% tax on entire turnover for non-compliance in some cases

-

Scrutinized on-chain data and foreign exchange transactions

Traders must now justify why TDS wasn’t applied to their foreign trades or face severe penalties.

ALSO READ: Now Open: Pan-India Registration for Fraud Investigators!

Industry Reaction

According to Vikram Subburaj, CEO of Giottus (a local crypto exchange), this regulatory backlash was inevitable: “Exchanges that bypass TDS are putting Indian traders in a difficult position. Traders should respect and follow the law of the land.” Many believe the responsibility of TDS compliance lies with traders when using foreign platforms, although ambiguity remains.

Tightened Withdrawals from Domestic Exchanges

Over the last 18 months, Indian exchanges have made crypto withdrawals more difficult, fearing money laundering and tax evasion.

This has encouraged traders to:

-

Withdraw coins to foreign wallets

-

Swap coins offshore

-

Engage in P2P transfers to bypass local controls

Concerns and Implications

Regulators are worried about:

-

Capital flight via unmonitored wallets

-

Undisclosed income and lack of tax trail

-

Use of crypto in illicit finance

-

Loss of control over crypto investments

Authorities may soon issue stricter compliance rules for traders using foreign platforms and expand monitoring of wallet-to-wallet movements.

As the I-T Department escalates its crackdown on crypto-related tax evasion, Indian traders using foreign platforms must brace for heightened scrutiny. With TDS compliance now firmly in the spotlight, the era of easy offshore crypto trading may be coming to an end.